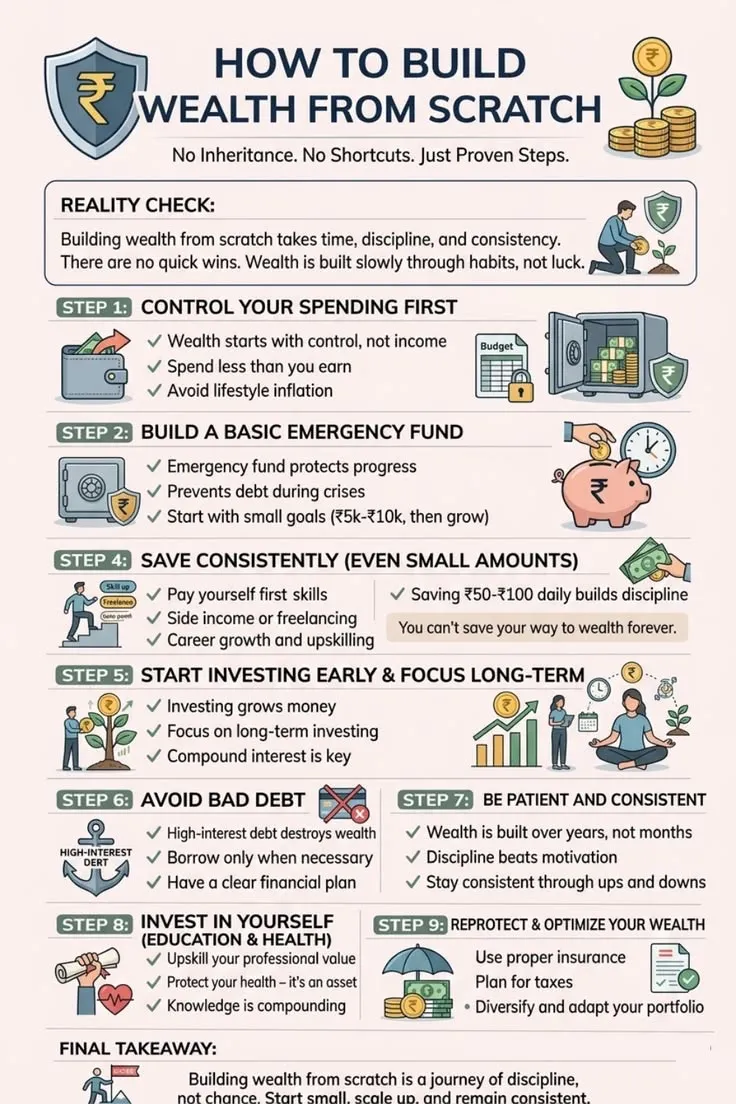

Financial stability is not built overnight. It develops through careful planning, disciplined saving, and smart financial decisions. One of the most important parts of personal finance is having a strong financial backup plan. A financial backup plan helps individuals prepare for unexpected situations such as medical emergencies, job loss, major repairs, or sudden family responsibilities without disrupting their long-term financial goals.

Many beginners believe they need a high income before creating a financial safety net. In reality, building a financial backup plan is more about developing consistent financial habits than earning a large salary. Even small savings made regularly can create meaningful financial security over time.

A well-structured backup plan provides peace of mind, reduces financial stress, and allows people to make better financial decisions during uncertain situations. This guide explains how beginners can start building a strong financial backup plan using practical and proven financial principles.

Understand What a Financial Backup Plan Means

A financial backup plan is a strategy designed to protect your finances during unexpected events. It acts as a safety net that helps cover essential expenses when regular income is interrupted or unforeseen costs arise.

Unlike short-term spending money, a backup fund is intended for genuine emergencies rather than planned purchases or entertainment. Its purpose is to maintain financial stability without relying on expensive borrowing or disrupting long-term savings and investments.

Understanding this distinction helps beginners use their financial resources wisely and avoid unnecessary financial pressure.

Evaluate Your Current Financial Situation

Before creating a backup plan, it is important to understand your current financial position. Review your monthly income, fixed expenses, variable expenses, existing savings, and any outstanding debts.

Tracking your cash flow helps identify how much money is available for regular savings after covering essential needs. It also highlights unnecessary spending that can be reduced to strengthen your financial plan.

Knowing your financial situation provides a realistic starting point and makes it easier to create achievable goals.

Set Clear Financial Goals

A strong financial backup plan should be connected to clear financial goals. These goals provide motivation and help determine how much money needs to be saved.

Short-term goals may include building an emergency fund or paying off small debts. Medium-term goals could involve saving for education, a vehicle, or home improvements. Long-term goals often include retirement planning, wealth creation, or financial independence.

Clear goals make financial planning more organized and help maintain consistency even when progress seems slow.

Create a Practical Monthly Budget

A monthly budget is one of the most effective tools for building financial security. It helps allocate income toward essential expenses, savings, and future priorities while preventing unnecessary spending.

A balanced budget includes housing, food, transportation, healthcare, utilities, debt repayments, and savings. Instead of saving whatever remains at the end of the month, many financial experts recommend treating savings as a regular monthly expense.

Following a realistic budget allows beginners to gradually strengthen their financial backup plan without making drastic lifestyle changes.

Build an Emergency Fund Gradually

An emergency fund is the foundation of every financial backup plan. It provides immediate financial support during unexpected situations such as job loss, medical emergencies, urgent home repairs, or sudden travel needs.

Building this fund does not require large deposits immediately. Regular contributions, even in small amounts, help create meaningful savings over time.

Keeping emergency savings separate from everyday spending accounts reduces the temptation to use the money for non-essential purchases and ensures that it remains available when truly needed.

Develop the Habit of Saving Consistently

Consistency is more important than the amount saved in the beginning. Establishing a regular saving habit builds discipline and supports long-term financial growth.

Automatic transfers to a savings account can simplify the process and reduce the likelihood of skipping contributions. Saving immediately after receiving income also helps prioritize financial security over unnecessary spending.

Small but consistent savings often produce better long-term results than occasional large deposits.

Reduce Unnecessary Expenses

One of the easiest ways to strengthen a financial backup plan is by controlling unnecessary expenses. Many people spend money on subscriptions, impulse purchases, or lifestyle upgrades that do not significantly improve their quality of life.

Reviewing monthly expenses helps identify areas where spending can be reduced without affecting essential needs.

Redirecting these savings toward emergency funds or long-term financial goals accelerates progress and improves financial stability.

Manage Debt Responsibly

Debt can slow financial progress if it is not managed carefully. High-interest debt, in particular, can reduce the amount of money available for savings and investments.

Creating a repayment strategy helps reduce financial pressure and improves long-term financial health. Paying installments on time also helps avoid additional interest and penalties.

Responsible borrowing and careful debt management allow beginners to focus more effectively on building financial security.

Protect Yourself With Appropriate Insurance

A financial backup plan should also include protection against unexpected risks. Insurance can reduce the financial impact of accidents, health emergencies, or property damage.

Choosing appropriate insurance coverage based on personal needs helps prevent major financial setbacks. While insurance does not replace emergency savings, it works alongside them to create a more complete financial safety net.

Understanding available protection options is an important part of responsible financial planning.

Learn Basic Investment Concepts

Once a stable emergency fund has been established, beginners can gradually learn about investing to support long-term financial goals.

Investing allows money to grow over time and can help protect purchasing power against inflation. However, investment decisions should always match individual financial goals, risk tolerance, and investment timelines.

Learning basic financial concepts before investing helps beginners avoid emotional decisions and unrealistic expectations.

Monitor and Review Your Financial Plan

Financial planning is not a one-time activity. Income, expenses, family responsibilities, and personal goals change over time, making regular reviews essential.

Checking your financial progress every few months helps ensure that your backup plan remains effective and aligned with your current situation.

Updating budgets, adjusting savings targets, and reviewing financial priorities allow your plan to remain practical as circumstances evolve.

Avoid Common Financial Mistakes

Many beginners delay creating a backup plan because they believe they do not earn enough money. Others rely too heavily on credit cards or ignore emergency savings entirely.

Additional mistakes include failing to track expenses, making impulsive purchases, investing without adequate knowledge, and neglecting financial planning altogether.

Recognizing these common mistakes early helps build stronger financial habits and supports long-term stability.

Improve Your Financial Knowledge

Financial literacy plays a key role in making informed money decisions. Understanding budgeting, saving, investing, debt management, and financial risk helps individuals make better choices throughout life.

Reading reliable financial resources, attending educational programs, and staying informed about personal finance concepts can improve confidence and decision-making.

Continuous learning strengthens financial independence and supports long-term success.

Benefits of Having a Financial Backup Plan

A well-prepared financial backup plan offers numerous advantages beyond emergency protection. It reduces stress during unexpected situations, improves financial confidence, and allows people to make decisions without constant financial pressure.

Individuals with strong financial reserves are often better prepared to handle career changes, family responsibilities, or economic uncertainty. Financial security also creates greater freedom to pursue personal and professional opportunities.

Building a backup plan is therefore an investment in both financial stability and overall peace of mind.

Frequently Asked Questions (FAQs)

Why is a financial backup plan important?

A financial backup plan helps cover unexpected expenses, reduces financial stress, and protects long-term financial goals during emergencies.

How much should beginners save for emergencies?

The ideal amount depends on personal circumstances and monthly living expenses. Building savings gradually through regular contributions is the most practical approach.

Can I start a financial backup plan with a low income?

Yes. Financial backup plans are built through consistent saving habits, budgeting, and careful money management rather than high income alone.

Conclusion

Building a strong financial backup plan is one of the most valuable steps beginners can take toward long-term financial security. It provides protection against unexpected events while creating confidence and stability for the future.

By understanding your financial situation, creating a realistic budget, saving consistently, managing debt responsibly, and improving financial knowledge, you can establish a reliable financial safety net that supports both your present needs and future goals.

Financial success is rarely the result of a single decision. It is built through consistent habits, thoughtful planning, and a commitment to making informed financial choices every day.