Starting a career is an exciting milestone, but it also brings the responsibility of managing money wisely. In 2026, young professionals are facing a financial environment shaped by rising living costs, rapid technological changes, evolving investment opportunities, and increasing digital financial services. Building strong financial habits early can help individuals achieve long-term stability, reduce financial stress, and create opportunities for future growth.

Financial planning is not just about saving money. It involves setting realistic goals, managing expenses, building emergency savings, investing wisely, protecting against financial risks, and making informed decisions that support both present and future needs.

Whether you have just started your first job or are a few years into your career, creating a financial plan can help you gain confidence and control over your finances. This guide explains practical financial planning tips that young professionals can use to build a secure financial future in 2026.

Understand Your Financial Situation

The first step in financial planning is knowing exactly where you stand financially. Many young professionals receive a salary but may not fully understand how much they earn, spend, save, or owe.

Begin by reviewing your monthly income, fixed expenses, variable expenses, outstanding loans, and current savings. Tracking your cash flow helps identify unnecessary spending and highlights opportunities to improve your financial habits.

A clear understanding of your financial position provides the foundation for making smarter financial decisions.

Set Clear Financial Goals

Financial goals provide direction and motivation. Without specific goals, it becomes difficult to decide how much to save or where to invest.

Short-term goals may include building an emergency fund, purchasing essential items, or paying off small debts. Medium-term goals could involve buying a vehicle, pursuing higher education, or making a down payment on a home. Long-term goals often focus on retirement planning, financial independence, or wealth creation.

Writing down your goals and reviewing them regularly increases your chances of achieving them.

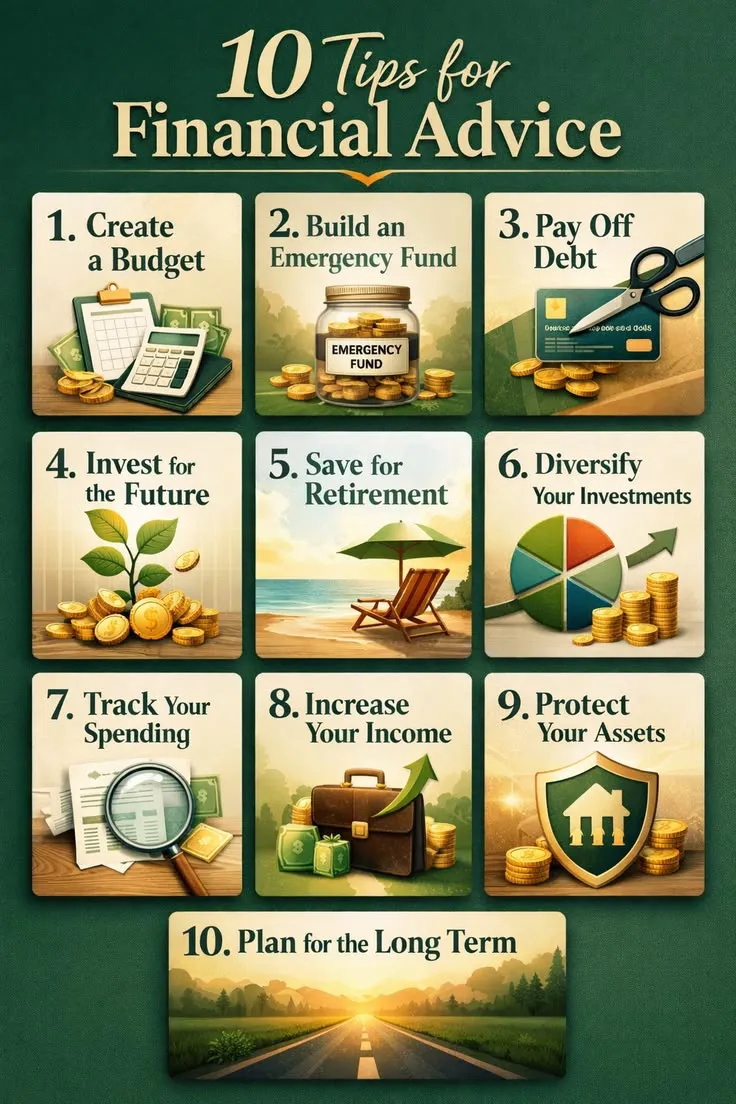

Create a Monthly Budget

A well-planned budget helps you control spending while ensuring that essential expenses and savings remain priorities.

Your monthly budget should include housing, transportation, food, insurance, utilities, debt repayments, savings, and personal spending.

Instead of treating savings as money left over after spending, consider saving first and planning the remaining expenses around your available income.

A realistic budget creates financial discipline without making daily life unnecessarily restrictive.

Build an Emergency Fund

Unexpected events such as job loss, medical emergencies, or urgent repairs can disrupt financial stability.

An emergency fund provides financial protection during difficult situations without forcing you to rely on loans or credit cards.

Financial experts generally recommend building emergency savings that can cover several months of essential living expenses. However, beginners should focus on building the fund gradually rather than feeling pressured to reach a large amount immediately.

Consistent saving is more important than the initial size of the fund.

Avoid Lifestyle Inflation

As income increases, many young professionals naturally increase their spending. This behavior, often called lifestyle inflation, can slow long-term financial progress.

Instead of spending every salary increase, consider directing part of the additional income toward savings, investments, or debt repayment.

Maintaining reasonable spending habits while income grows allows wealth to accumulate more effectively over time.

Balancing enjoyment with responsible financial planning creates long-term benefits.

Manage Debt Responsibly

Loans and credit products can support important life goals, but excessive borrowing may create financial pressure.

Understanding interest rates, repayment schedules, and borrowing costs helps individuals make informed decisions.

Paying bills on time, reducing high-interest debt, and avoiding unnecessary borrowing improves financial stability.

Responsible debt management also supports a stronger financial profile for future borrowing needs.

Start Investing Early

One of the greatest advantages young professionals have is time. Starting investments early allows long-term growth through the power of compounding.

Investment decisions should match personal financial goals, time horizons, and risk tolerance.

Diversifying investments and maintaining a long-term perspective can help reduce risk while supporting wealth creation.

Before investing, it is important to understand basic investment principles and avoid making decisions based on emotions or short-term market movements.

Protect Yourself With Insurance

Financial planning also involves protecting your income and assets against unexpected events.

Health insurance, life insurance, and other appropriate coverage can reduce financial risks associated with accidents, illness, or family responsibilities.

Insurance complements savings by preventing major financial setbacks during emergencies.

Selecting suitable coverage based on your personal situation strengthens your overall financial plan.

Improve Financial Knowledge

Financial literacy is one of the most valuable investments young professionals can make.

Understanding budgeting, taxation, investing, retirement planning, and personal finance concepts helps improve decision-making.

Reading reliable financial resources, attending educational programs, and staying informed about financial developments can build confidence over time.

Continuous learning allows individuals to adapt to changing financial environments.

Plan for Retirement Early

Retirement planning should begin much earlier than many people expect.

Starting early allows investments more time to grow and reduces the amount needed to be saved later in life.

Even modest contributions made consistently over many years can create significant retirement savings.

Including retirement planning in your financial strategy from the beginning supports long-term financial independence.

Use Digital Financial Tools Wisely

Modern financial technology has made money management easier than ever.

Budgeting apps, digital banking platforms, investment tools, and expense trackers help users monitor spending, automate savings, and organize financial information.

While these tools provide convenience, they should support informed financial decisions rather than replace financial discipline.

Technology works best when combined with good money management habits.

Review Your Financial Plan Regularly

Financial planning is an ongoing process rather than a one-time activity.

Changes in income, career growth, family responsibilities, or economic conditions may require adjustments to your financial strategy.

Regularly reviewing your budget, savings progress, investments, and financial goals helps ensure that your plan remains effective.

Flexibility allows you to adapt to new opportunities and unexpected challenges.

Avoid Common Financial Mistakes

Many young professionals delay saving because they believe they have plenty of time. Others spend beyond their means, ignore emergency savings, or make investment decisions without proper research.

Another common mistake is relying too heavily on credit cards or postponing retirement planning.

Recognizing these mistakes early can help build stronger financial habits and improve long-term financial outcomes.

Good financial decisions made today often produce significant benefits in the future.

Maintain a Healthy Balance Between Saving and Living

Financial planning does not mean avoiding all enjoyment or spending.

A balanced approach allows individuals to enjoy life while remaining committed to long-term financial goals.

Responsible spending, regular saving, and thoughtful investing create a sustainable financial lifestyle.

The objective is not simply to accumulate money but to build financial security while maintaining a good quality of life.

Frequently Asked Questions (FAQs)

Why should young professionals start financial planning early?

Starting early allows more time to build savings, invest for long-term growth, and prepare for future financial goals.

What is the first step in financial planning?

The first step is understanding your current financial situation by tracking income, expenses, savings, and debts.

How much should young professionals save every month?

The amount depends on individual income and expenses, but consistent saving is more important than the exact percentage.

Conclusion

Financial planning is one of the most valuable skills young professionals can develop in 2026. A well-structured financial plan helps individuals manage expenses, build emergency savings, invest wisely, protect against risks, and achieve long-term financial goals.

By creating a realistic budget, avoiding unnecessary debt, improving financial knowledge, and maintaining disciplined saving and investing habits, young professionals can establish a strong financial foundation for the future.

The earlier financial planning begins, the greater the opportunities for long-term success. Consistent habits, informed decisions, and regular reviews can help create financial confidence and lasting financial security throughout every stage of life.